Rookie Series Article 2: Big Banks Are Bad For Your Wealth, Part 2

To continue from Part 1, I show how banks use your money to make themselves wealthy, while leaving you in the dust. In Part 1, I discussed how big banks charge you to do business with them. In this part, I explain how big banks skimp on paying you for helping them grow their own wealth.

Big Banks Give You The Smallest Piece of the Pie

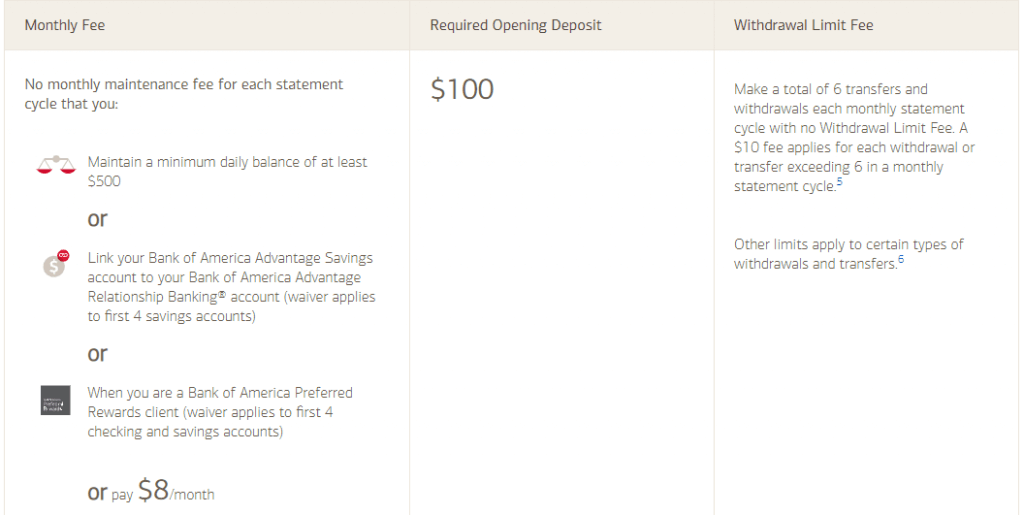

Once again with savings accounts, big banks charge you to use their service, unless you meet the minimum requirement. In the below photo, the fees are waived if you meet certain requirements. Similar to overdraft fees from the checking account, banks make money off your ability to move your money. If you are planning on sitting this money, then you have nothing to worry about. This withdrawal limit is one of the key differences between savings accounts and checking accounts.

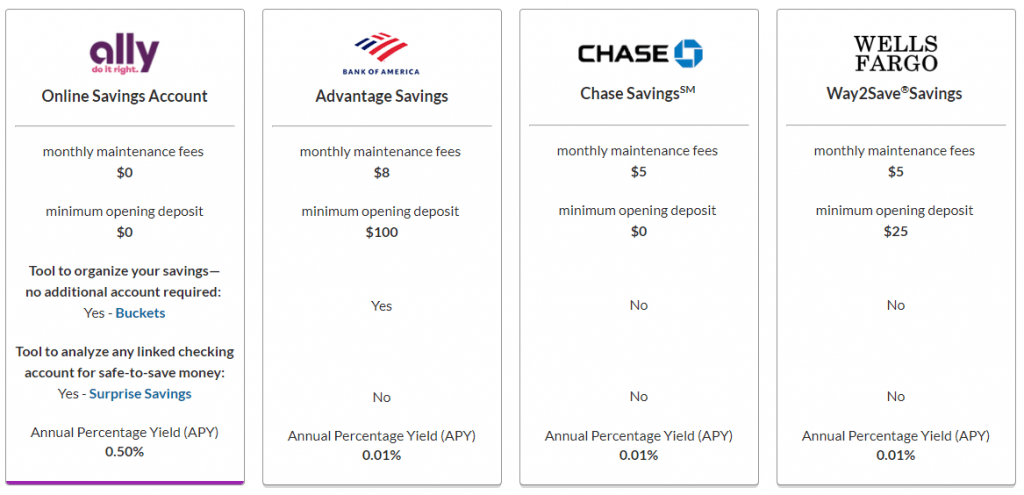

The next, and probably largest difference between checking an savings is the interest rate. This is the money the bank is paying you over time for parking your money in the checking account. “This is it! This is where I build my wealth!” Well, not so fast. Lets look at how big banks compared to a popular online bank.

As you can see above, the interest rate on an online savings account is 50x higher than those from the big banks. Not only this, there are no monthly fees or no minimum balances. This is clearly a better option, but not many people do research to find different interest rates that would work best for them. In future articles, I will explain how the APY works and how compounding can be your best friend or worst enemy, depending at which angle you’re looking at it.

Story Time!

Another college story. College Matt started his banking with Washington Mutual (yes, dating myself). This bank was notorious for not charging a withdrawal fee from their checking accounts at various ATMs (This is important and maybe I’ll cover this later). To make things convenient, I started a savings account with them as well. In the financial crisis, Chase bought Washington Mutual, so I was grandfathered in. On my $1,000 I had in my savings account, I was receiving 0.01% APY, meaning every year i made 10 cents. Watch out ladies! At that time, the interest rates were high and I had heard about Ally. At that point, they were at 2% APY (rates fluctuate with the economy). Now, instead of making 10 cents, I was making $20 on the funds in the savings account. This is WAY better.

{kind=link}