This Market is Wild

Right now is a wild time in the world. The pandemic is still going crazy, the housing market is skyrocketing, and the supply chain is struggling to meet demand. There is also huge inflation fears. So, today, I wanted to break down a few pieces of the economy that will help you become well informed on the market to guild some future decisions.

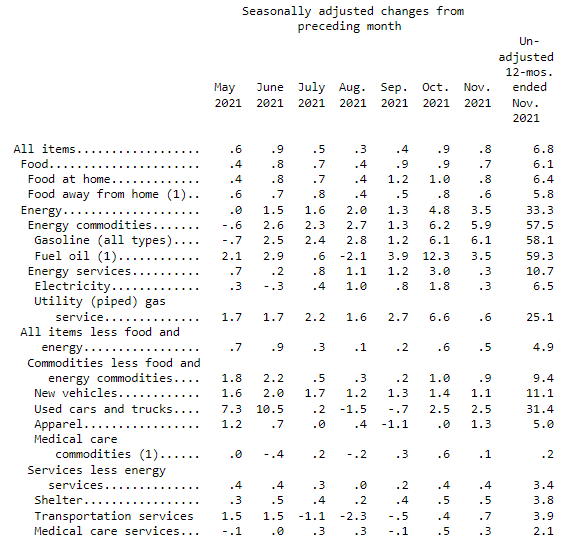

Consumer Price Index (CPI)

Before we talk about why the Consumer Price Index (CPI) is where it is, let’s quickly talk about what makes up the CPI. The CPI is comprised of commodities that change in price and are not dictated by the wealth of the individual. For example, real estate, stocks, and other investments are not included. It focuses instead on things like milk, eggs, bread, etc. It doesn’t matter how rich you are, you’re not going to buy more eggs than you need, driving up prices.

As you can see in the following table, there are categories that are increasing over the past year. The numbers are shown in a percentage and the overall price change is 6.8%, meaning inflation this year was 6.8%. Makes sense right? There are many things that contribute to the price growth. But, the largest contributions are the pandemic and supply issues. Let’s get into the supply and how it effects the CPI.

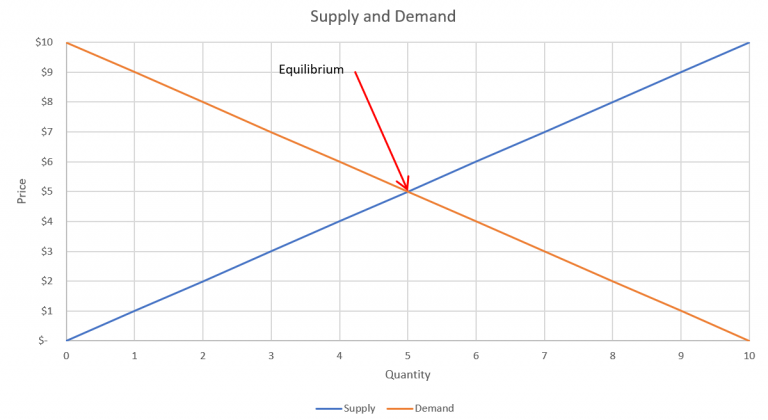

Supply and Demand

Supply and demand are basic economic terms that play a huge part in the economy. Typically, the price is set by an equilibrium point where the supply meets the demand. Now, looking at the supply, when the supply gets constrained and the cost to produce the next quantity increases, the curve shifts up, driving the price up. On the demand side, when the need for a quantity increases, then the demand shift goes up, also increasing the price of the equilibrium.

Supply Chain Shortage

Probably everyone has seen the pictures of the Port of Los Angeles with ships waiting in the harbor to unload. This has obviously led to things not being delivered on time. But, the true reason behind the shortage is further back in the supply chain. Let’s dive a little deeper.

Pandemic Panic

When the pandemic started, many companies thought the demand was going to drop so significantly, so they cut their orders. The thought was that we were all going to be on lock down for an unknown amount of time and we wouldn’t want to buy goods. As we know, that was not the case, but the logic was sound. Why go buy a new car if you aren’t driving to work, right? Well, what actually happened was quite different. People still bought as usual, plus, with the multiple stimulus checks, they bought even more. And, just like that, the supply was gone.

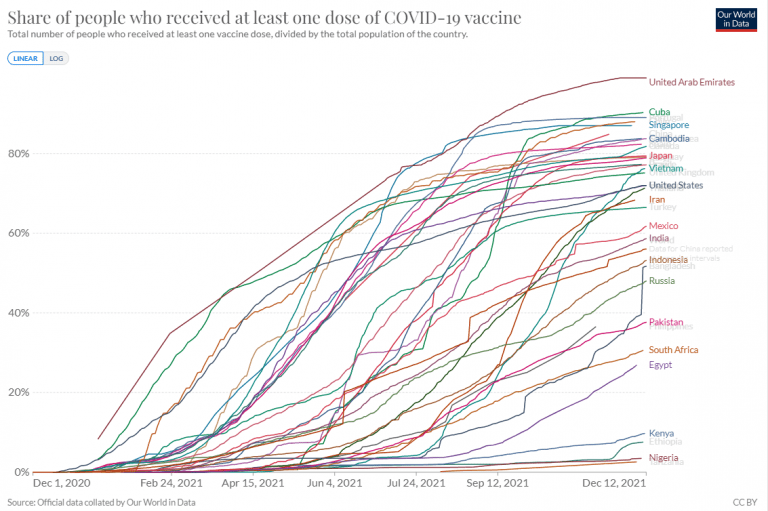

Vaccine Shortage

Now, I know what you’re thinking, how can there possibly be a vaccine shortage, especially when a good chunk of the US refuses to get one? Well, in many third world countries, they don’t have that luxury. These countries include South East Asia. And, where do you suppose the factories for many projects are located? That’s right, South East Asia. Until the pandemic is under control in those areas, factories will continue to be at limited capacity and product shortages will continue.

Housing Market

The housing market is also a product of supply and demand, but coupled with historically low interest rates. First, much like the other companies, construction companies thought people were going to stop buying houses during the pandemic, so they slowed production. This assisted in a housing shortage. According to realtor.com, America is short 5.24 million homes. This is causing prices to jump. Plus, though prices are increasing, many aren’t selling because they wont have a new house to move into. This adds to the problem of a decreased shortage. Meanwhile, as the building sped back up, the lumber prices shot up, causing housing construction costs to jump with it.

It has never been cheaper to borrow money. To illustrate this point, someone who can only afford to pay $2,000 a month. At a 5% interest rate, the individual would be able to afford a $375,000 house. However, at a 3% interest rate, they would be able to afford a $475,000 house. With the job market the way it is with companies offering more pay to get/keep employees, the average person is making more and can now get more house for their money.

Hedge Against Inflation

As I said, there is no better time to borrow money. The one good thing about borrowed money is as the value of money decreases, the debt amount stays the same. So if you took out a $10,000 loan today, next year with the 6.8% inflation, your debt, if unpaid would be equivalent to $9,942. So, if you used borrowed money to purchase income producing assets, like real estate or in the stock market, you could make that money work for you. Let’s say the investment matched inflation, at 3% interest on the loan, you would make 3.8% on that money. Holding onto your money in these uncertain times makes your money slowly lose value.

Disclaimer

Once again, I am not a financial advisor. These tips are some things I have validated with my own personal experiences. If you feel you need more personal advice, please consult a professional financial advisor. Dont forget to check out the Book List for published authors on this topic!