It's All About the Deal Analysis

We chose our target asset, narrowed down our target market, and now its time to do a deal analysis on a property. We talked to our mortgage broker to find our pre-approved amount, and we went hunting. You will need to analyze numerous properties before you find one that meets your criteria. Don’t be discouraged, you’ll find one. Here is how I built our deal analysis tool to find our first BRRRR.

Deal Analysis: Basic Inputs

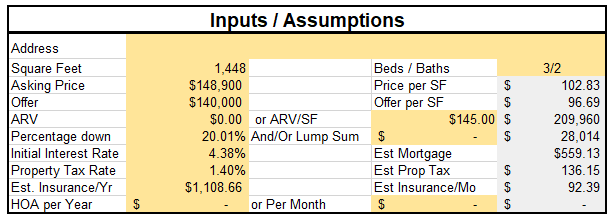

When first looking at a property, you need to start with the basics, if anything, just to get the info onto paper. Most of this information you can pull off websites like Zillow. Chances are, this is where you found the property to begin with. Off the cover page for the property, here are the key variables to note:

- Square Footage

- Asking Price

- Property Tax Rate

- Estimated Insurance

- HOA Fees (if applicable)

Most of the time this information is accurate, but I would still verify the square footage. Now that you have the easy information jotted down, now there is a bit of research needed for other inputs. The first thing to look at is the After Repair Value (ARV). This will tell you the value of the house. I’m sure you’re looking at Zillow and thinking “Too easy! There is a Zestimate.” If you were to take that to an investor or mastermind group, you’ll be laughed off the stage, so please don’t. The best way is to look at recently sold comps in the area. You can do this on Zillow, just change the search criteria to sold. Be realistic though. Don’t use the random mansion a couple neighborhoods over as a comp.

At times the comparables are easy, especially in cookie cutter neighborhoods. If you can find a couple with the same floor plan and turn key, then your job is easy! However, if you’re looking at older neighborhoods, it’s best to look at similar styles, bed/bath counts, and square footage. To get the most accurate numbers, I typically will use a cost per square footage. In the example above, this 1,400 square foot house had an ARV/SF of $280 bringing the ARV to $392,000 (1,400×280). As for the initial interest rate on your loan, it is highly recommend you talk to a mortgage broker to get preapproved before you get too deep into analyzing deals.

Note the grey column that is auto-populated. I highly recommend using either an online deal calculator. You can find these on BiggerPockets, for example, but you will have to pay after a couple of free samples. Or, if you’re like me, use Excel. You do run the risk of making a simple error that could throw off your numbers, but you’ll be able to see the inner workings, which is prefer. Hint: the mortgage calc is the =PMT() function.

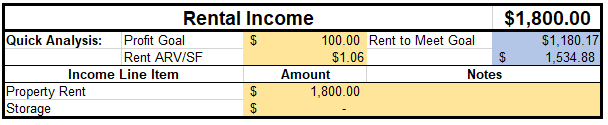

Deal Analysis: Expected Income

Now that we have the basic information about the property itself, it’s time to look at the rental market. Similar to how we developed the ARV, we need to review rental comps in the area. Again, you can do this research on sites like Zillow, Apartments.com, even CraigsList. The difference is there is less variability based on square footage. It’s more about bedrooms and bathrooms. Of course, square footage can’t be negated; however, being off by 50 square feet isn’t going to change rental values.

If you have a 3 bed/ 2 bath, look for others in the area. The closer proximity to the neighborhood with the same finishes the better. Remember, when considering your market, if you put A finishes in a C neighborhood, you’ll maybe get B rent. So don’t think putting granite countertops in a poor neighborhood will get you as much rent as the rich neighborhoods.

Remember to consider all potential income sources when looking at a property. If there is a granny flat, or a large storage in the back, it could be used for extra income, if that is typical in your area. Don’t try and charge extra for the garage on a single family house. It won’t go well.

Notice in the above breakdown, I have a quick analysis area. This is just something useful I build to help choose the appropriate rent. One is driven by me and the other by the market. The profit goal is saying how much profit I want to have based on the mortgage, escrow, and expenses, which I will get to next. The second part is determined by the market, but once again, this is a rough number because rents aren’t strongly determined by the square footage.

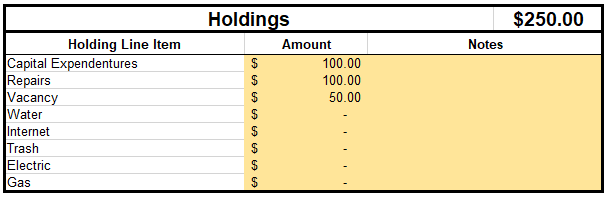

Deal Analysis: Projected Expenses

The projected expenses are those outside of the estimated mortgage and escrow payments found on the initial assumptions. When I say escrow, I mean property tax and insurance payments that you may elect to include with your mortgage payments. Anyways, the other expenses for the property are the property management expenses and the holdings. You may elect to manage the property yourself, but I would strongly consider a property manager. They save you time and headache. Below is my management assumptions.

The property management fees differ from manager to manager, and region to region. The most common I have seen is 10% a month of the income and 75% of the first month rent as a move-in initial fee. I distributed this cost across every month based on the rent we input. So, the 10% ($180) plus the 75% of the first month rent divided by 12 months ($1800 x 75%/12 months = $112.50).

The next category, holdings, is a list of expenses that are either current or future expenses. As for current expenses, you may have to pay tenant utilities. This is more common on multifamily housing, but some areas have landlords paying for trash. The future expenses are items that you want to set aside funds for when they do, and they will, arrive. This includes maintenance, vacancies, and capital expenses like a roof repair or furnace replacement.

Deal Analysis: Estimated Repairs

When I started doing analysis, I would estimate the repair cost based on the assumed condition of the property (through photos) and then multiplying the square footage by a dollar value. For example, if the property looked like it was in great condition, I’d multiply it by $10, but if it was in poor condition, I’d multiply it by $50. But, that is too wild of a guess for me. So, I read the Book on Estimating Rehab Costs and reached out to another BRRRR investor and developed a spreadsheet that had estimated costs based on repair types. Originally, when using the cost per square foot, the estimate I had was $36,200. And, after the breakdown with a 20% contingency, my estimate is $34,000, so not too far off.

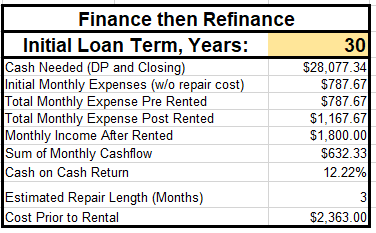

Deal Analysis: Cash Flow Analysis

Pre-Refinance

While running the renovation, as you can expect, there is no rental income. The expenses are mortgage, property tax, and insurance, which comes to $787.67 per month. We are paying cash for the repair, so we do not need to include interest payments on a renovation loan, but, if you’re using one, you will need to include required payments.

Once rented, our monthly income will be $1,800 with monthly expenses of $1,167.67 (mortgage, escrow, property management, and holdings). The cash flow for this property is $632.33. The cash needed to close plus the estimated repair is $62,085.34. This brings a cash on cash return of 12.22% per year. This is pretty good as is, but we’re planning for better.

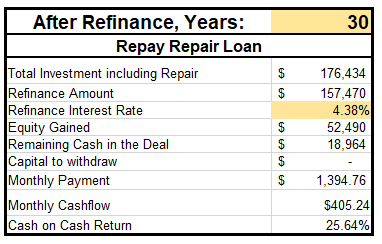

Post-Refinance

The goal of a BRRRR is to get as much money back as possible. In the initial assumptions, we found the ARV to be $209,960. If we are conservative and are able to get a 75% loan to value (LTV) for this amount, we would cash out refinance for $157,470. This would mean we would have to leave $18,960 in the property and gain $52,490 in equity. We are assuming the same rate on a new 30 year mortgage. The new monthly expenses increase to $1,394.76. The new cash flow is now $405.24. While this is a decrease of over $200 a month, with the decrease in the invested capital, the cash on cash return is 25.64%! This means the investment will pay itself back in under four years!

What's Next?

The deal analysis is critical to your real estate journey. The more you do these type of analyses, the more proficient you’ll be and the faster you’ll be able to plug and play information. The good news is we won the bid of under the asking price thanks to a great realtor, so now its time to get this property closed!

Disclaimer

Once again, I am not a financial advisor. These tips are some things I have validated with my own personal experiences. If you feel you need more personal advice, please consult a professional financial advisor. Dont forget to check out the Book List for published authors on this topic!

{kind=link}

{kind=link}