Financial Foundation to Start Your Path

Financial foundation building starts with getting control of your accounts. I accomplished this by creating an artificial zero in my checking account, moved my money to online savings accounts, set strict budgets, built credit, and eliminated bad debt. The following guilds will help you build your financial freedom moving forward. Check out the YouTube video that accompanies these suggestions!

Financial Foundation Pillar #1 Create an Artificial Zero

Financial foundation building starts with your bank account. As I said in previous posts, big banks are bad for your wealth. The largest scam in the banking industry is Overdraft Protection. I mean think about it. If you are so poor that you go negative in your account, they “help you out” by charging you $40?! Even if you go over by $1. That is the largest percent fee I have ever seen! When I was young, this fee burned me. No, I’m not talking about the adult toy in the story time. I did not understand the difference between available balance and actual balance. The overdraft fees pushed my account to negative $200. This may not seem like much to some, but for a poor college student, that hurt.

After I was beat down a bit, I came to an epiphany. I need to create an artificial zero in my account, so when I hit that point, I’m broke. At this point in my life, I had saved a little bit of money, so I set that zero to $1,500. If my available balance went below $1,500, I considered it that I had overdrafted my account. I needed to get income into my account before I could spend any more. That meant no eating out, going to drinks with friends, or going to the movies. I was broke. After I came to that realization, I never even came close to the actual zero again.

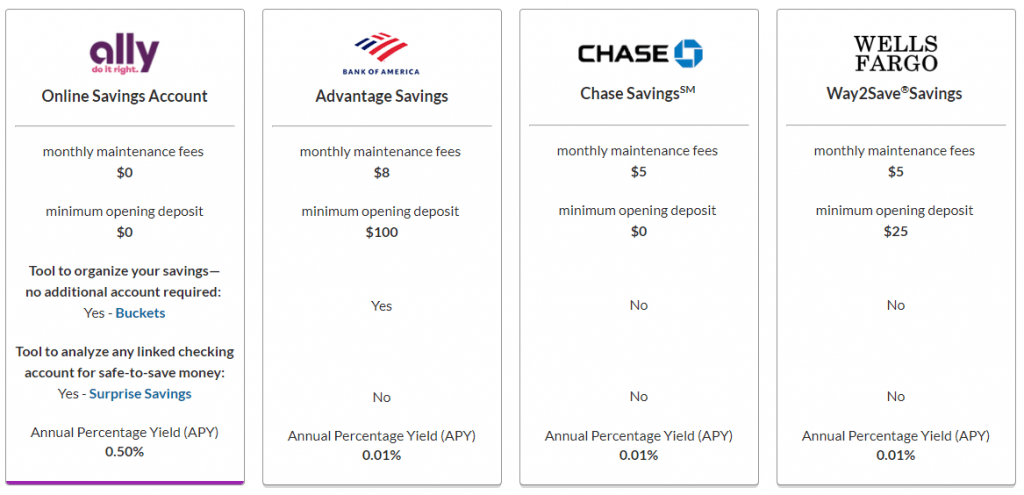

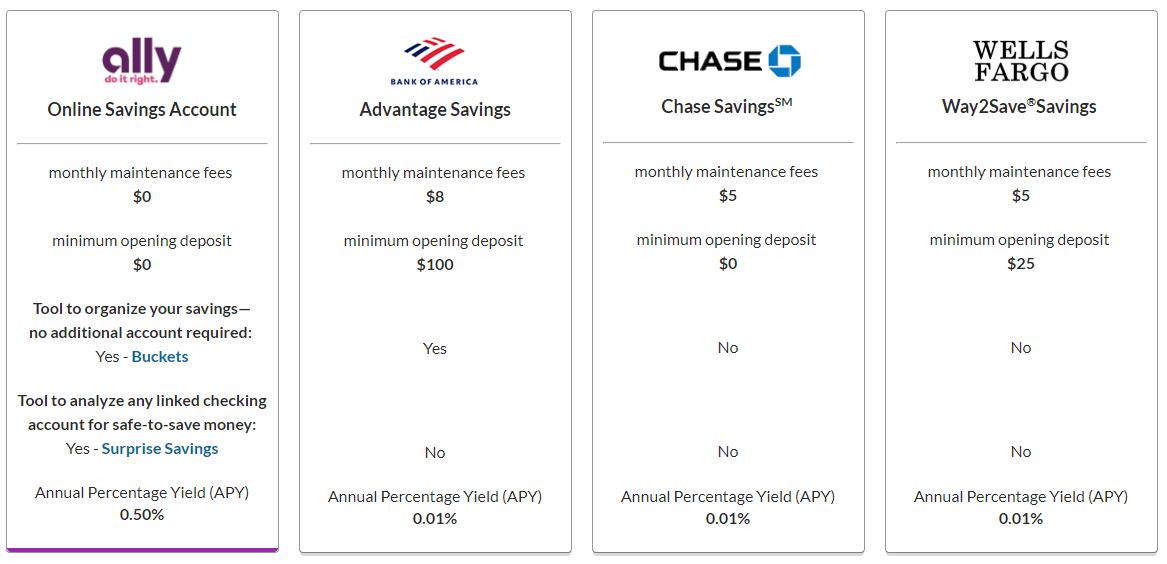

Financial Foundation Pillar #2 Start an Online Savings Account

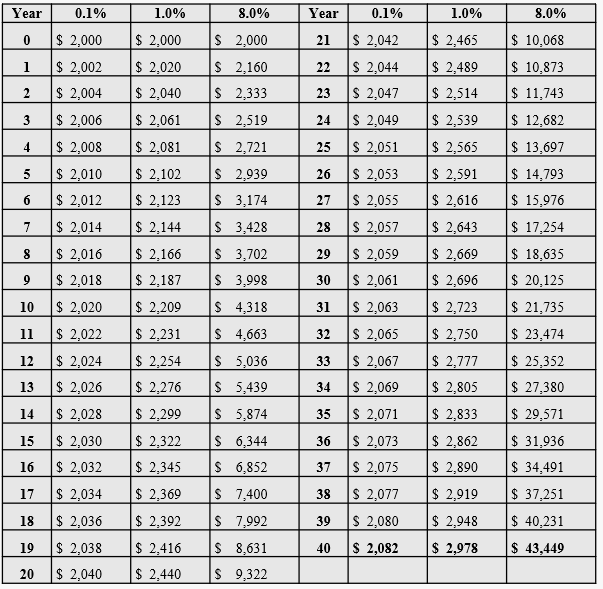

Now that you have control of your checking account, the next step is creating a savings account that will earn more for your parked money. As I said in previous posts, interest rates for big banks are atrocious. They give hundredths of a percent where online banks give up to 2% back on the money in the accounts. As we saw with compounding, that difference in the APY can equate to thousands of dollars in the long run.

A couple of the best online banks I have found are Ally and American Express FSB. They are typically 50 times the interest rate of the big banks. Remember, there are withdrawal limits to savings accounts, so you cannot use this account as your primary account to pay for things; however, there are local credit unions that often have interest producing checking accounts. This is another way to make money off your parked accounts.

Financial Foundation Pillar #3 Set up Budgets

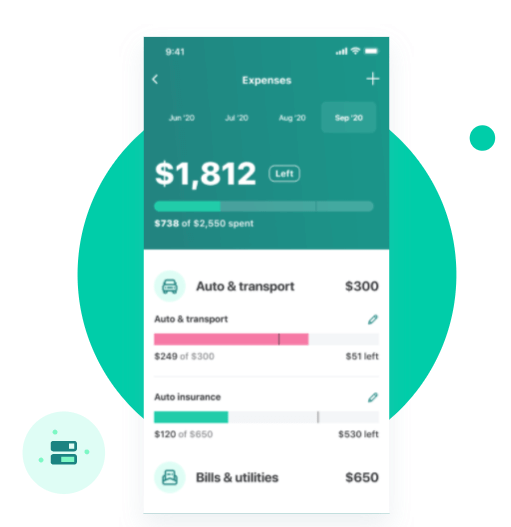

I’m sure you have heard this before. Setting up budgets are a great way to help you control your spending and build your financial foundation. Of course, that is assuming you can control yourself. Also, do you know how to set up budgets? One thing people do is create a simple spreadsheet that tracks how much your spending compared to the amount you allocated. This can be labor intensive in my opinion. But, if it works for you, then please do it! Another method I have seen is the envelope method. This method was made famous by Dave Ramsey. This works by putting cash in marked envelopes each month. Once you have exhausted that envelope, you’re done for the month in that category.

My favorite method that I still use today is Mint.com. This website, owned by Intuit, lets you link all of your accounts so you can track and categorize your spending, set savings goals, and, most importantly, set budgets. The beauty of these budgets is that if you go overbudget, you will get an email telling you that you went over. It is a digital kick to the gut if you’re over your restaurant budget by Cinco de Mayo. The budgets can also be adjusted based on previous spending habits to give you realistic spending patterns. I highly recommend it.

Financial Foundation Pillar #4 Build a Credit History

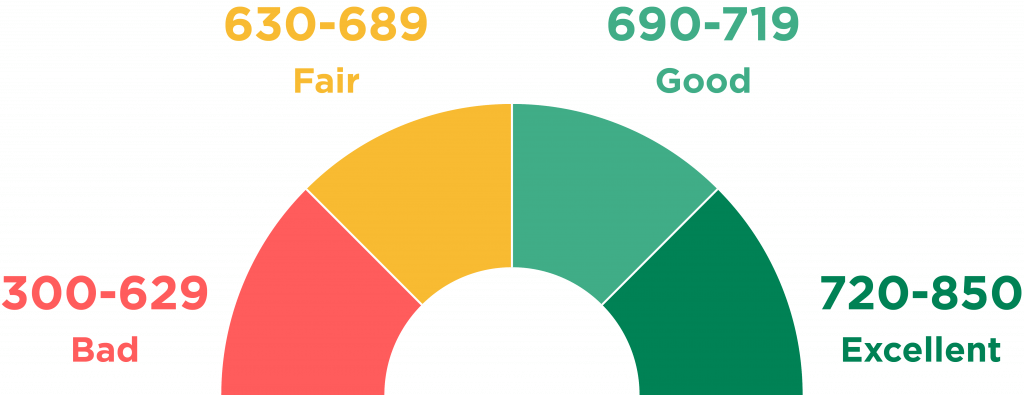

Credit is incredibly important, and if not used correctly, can really hurt you in the long run and crack your financial foundation. Many people look at the credit score and think “this is it, I have a good score, so I’m good.” This is incorrect. The credit score is the shell of you credit. The credit score provides a quick glance representation of you and your credit worthiness. But, much like a shell of a car, it doesn’t give a full picture of your entire credit. Creditors look at credit history, available credit, and number of accounts as well to determine if you are credit worthy. I will go into credit more at a later date, but for now, just know credit is important.

One of the pieces of the credit puzzle is credit history. The sooner you can start building a credit history, the better it will look in the future. There are many ways to do this. One of the safest ways is through a Savings Builder loan. What this does is creates a secure loan that you’re unable to touch. When I was getting started, I put the savings builder loan into my savings account and paid it off each month for a year. It cost me the interest payments, yes; however, the increase in my credit rating way worth every penny. Plus, I received interest on the money parked in my account, so it took the edge off. This is just one example of tools you can use to build your credit.

Financial Foundation Pillar #5 Consolidate Debt

This last piece of creating a base is to minimize existing debt. This could be from credit cards, car payments, personal loans, or any other outstanding balance on your books. Many of these debts have high interest rates. As we saw with the savings accounts, high interests rates add up to large amounts of money. In this case, the interest rates hurt. There is a method some people use where they front load extra payments onto one credit card to get it paid off fast. Once paid off, they add that payment to the next card to get that next one paid off fast. This snowballs until all debt is gone.

Another method that could be used to get rid of debt is a personal loan to consolidate all of the debt into one payment. Many loans will have a lower interest rate than the credit cards they will be paying off. This way you have a set payment each month that you could organize to pay off quickly. Of course doing this, you will now have credit cards with no balance. This does not mean you can go on a shopping spree. Credit cards can be used for a lot of good, another future article; however, in this situation, get yourself debt free before you allow yourself to make a big purchase using credit.

Disclaimer

Once again, I am not a financial advisor. These tips are some things I have validated with my own personal experiences. If you feel you need more personal advice, please consult a professional financial advisor.

{kind=link}