Make Your Money Grow Now

In the book, Rich Dad Poor Dad, the thing that separated the rich from the poor is how they viewed money. The poor worked for money and the rich had money work for them. You have acquired extra money and now you want it to work for you. Let’s look at some of the ways you can make your money grow and work for you.

Make You Money Grow With Savings Accounts

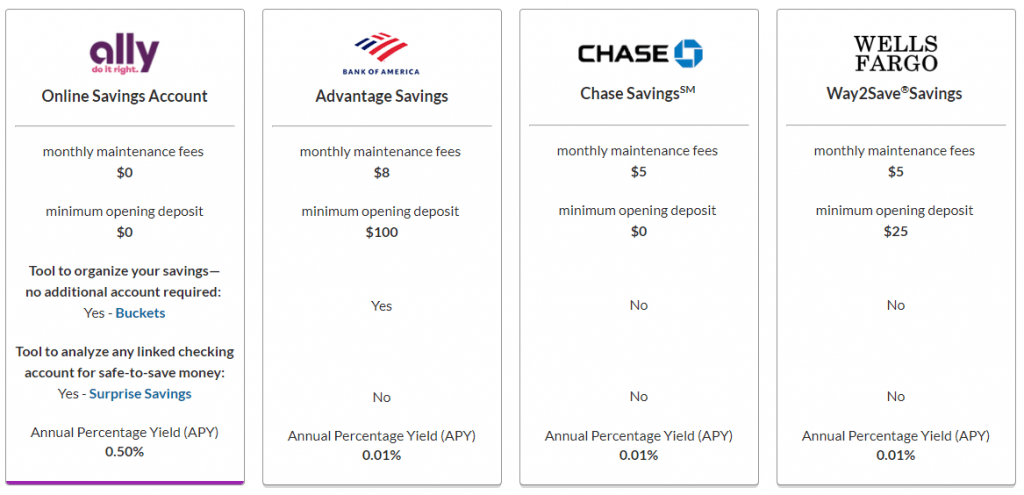

Reaching all the way back to my first posts, big banks are bad (and part 2), especially for savings accounts. They offer almost nothing for interest. With the big bank savings accounts, you might as well just leave the money in your checking account. You’re not going to make your money grow. If anything, with inflation, you’re losing money. Using online savings accounts instead, you can grow your money 50x faster than with a big bank. Yes, the current interest rates still don’t match inflation, but savings accounts are a low risk, highly liquid way to grow your money. This is typically advised for rainy day funds, when you’re close to a big purchase, or close to retirement.

Make Your Money Grow With Real Estate

Every wealthy person in the US has their hand in real estate. This is for good reason. It is an appreciating asset that can create huge cash flows as it grows in value. Yes, this may seem daunting at first, because the common conception is it takes a lot of money to go into real estate. There are many ways around the large 20% down payment that people think they need. You can house hack (rent out a room or half of a duplex). There is the BRRRR strategy, where you build equity into the property. Or, you can have the property be your primary residence, so you can put down a lower down payment and payoff your mortgage every month instead of someone else’s.

Make Your Money Grow With Stock Investments

This can of worms is a lot larger than just investing in stocks. There is a lot of aspects to this that depend on your want for control and liquidity. The first step is to get a brokerage account. I recommend Robinhood as your first app. It is easy to use without too many bells and whistles you get from other brokerages. Plus, they give you free stock when you start an account with them. It will help with understanding how stocks work.

Individual Stock Investing

Individual stock investing has numerous strategies. You can go for growth, value, momentum, or dividends. I break down these strategies in my previous post and how I use them in combination with each other. You can invest in individual companies or you can look in ETFs. Point being, you have direct control on where exactly your dollar goes. The liquidity with individual investing is not too bad. Typically, it takes a few days to transfer money from your brokerage account to your bank account. As with all investments, there is a good amount of risks. As we saw in 2008, the market can fall fast. But, as we saw after the start of COVID, the market can dig itself out of the hole fast. If you follow smart investing techniques and metrics, there should be good wealth potential.

Mutual Funds

Mutual funds are great for those that want to diversify their portfolio with minimal funds. As nice as it would be to own one share of Tesla, Amazon, Apple, and Google, that would cost a few thousand, and you only have four shares total. If you don’t understand mutual funds, check out this post. In essence, mutual funds are a group of investors that invest in a pool of funds that are managed by a funds manager. There is a bit of control, however, because you can choose the type of fund. Is it the retail sector, energy sector, or follow ETFs? You have control in the big picture portfolio. But, the composition is dictated by the fund manager.

Individual Retirement Accounts

Individual Retirement Accounts (IRA) are investment accounts similar to mutual funds. Often times they are used to invest in funds with very minimal expenses from the funds manager. The beauty of these accounts lies within the tax requirements. If you have a Roth IRA, then you put your post tax money into the account. After you retire and you withdrawal the money, you’re not taxed on that amount. If you have a traditional account, you’re not taxed before investing, therefore, you’re taxed after you withdrawal your profits. Both have their advantages. These accounts, if done through your employer, typically have funds listed as C-Funds, S-Funds, or G-Funds. This gives even less control than mutual funds, but you dont have to worry much. Just give your money to the professionals and let them do their thing. Remember, you cant touch this money until you retire. Otherwise, you’ll pay massive penalties.

Very Top Level Approach

Keep in mind that this is a very top level, general approach on these topics. There are ways you can use your IRA to invest in mutual funds and real estate. You can invest in stocks that equate to investing in real estate. There are also different methods of real estate investing, not just residential. Take this as the first step in your journey.

Disclaimer

Once again, I am not a financial advisor. These tips are some things I have validated with my own personal experiences. If you feel you need more personal advice, please consult a professional financial advisor.

{kind=link}

{kind=link}

{kind=link}