Mortgage Brokers Are Useful

Mortgage brokers save you time, money, and piece of mind. This is the reason they’re part of your Core Four. They have resources that can give you the best deals in lending markets that you may not have access to. So, having a broker will expand your pool of lender to almost guarantee the best deal. Of course, this may come at a cost. But, it is up to your keen eye to make sure the broker is working on your behalf and shares a similar agenda, get you the best deal! There is a reason the broker is part of your Core Four with a realtor, general contractor, and property manager.

Mortgage Brokers Do What?

A mortgage broker is your agent when it comes to finding the best terms and rates for your home loan. They have instruments that the public that does not to find companies that will provide you with a loan. So, these are you agents for getting the best bang for your buck! Additionally, they collect all the required information and documentation required by the lender. They will also be the voice of your funds to get the deal closed properly.

Mortgage Brokers Save You Time and Money

Like I said, these are your agents for shopping for the best deals. If you were to shop around on your own, where would you go? I bet you would probably start with big banks and go from there. I mean, you have heard that your bank does home loans, so why not have your loan on the same home page as your checking account? The problem is many big banks do not know your specific local market, or they just have blanket fees. There are other smaller companies or companies that specialize in mortgages that will provide you better rates, you just need to find them. So, the mortgage broker can do all of that for you, especially since they know where to go.

Mortgage Brokers Provide Personalized Service

If you have a good mortgage broker, they will not only work with you to get you the best deal, but they will also walk you through everything to help you understand the fine details. There are fees that come with any mortgage and they are shown in the closing costs breakdown. The interest rate alone is not always a deciding factor. Some times the closing costs are so high that the lower interest rate cost you more money. So, having a mortgage broker on your team will identify these pitfalls to get you into the best mortgage.

How Mortgage Brokers Get Paid

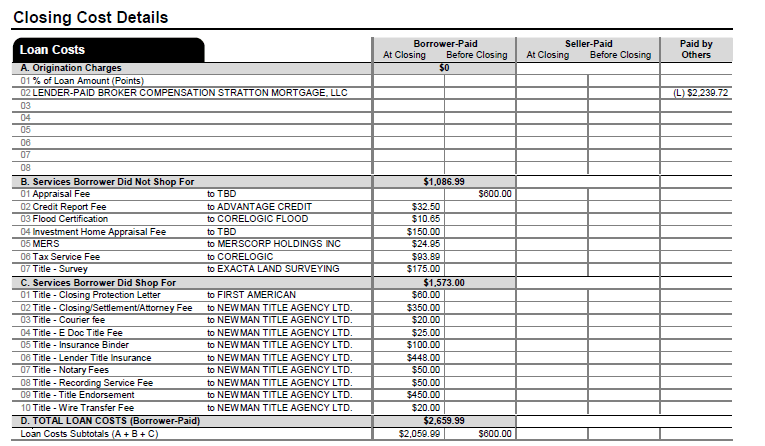

Mortgage brokers are paid one of two ways. First, there is Borrower Paid Compensation. This type of compensation is where the borrower (you) pays a direct fee. On the closing costs, under Origination Charges, you would see a line item titled “Borrower-Paid at Closing.” The other type of compensation is Lender Paid Compensation. Lender Paid Compensation is set quarterly with lenders and, therefore, non-negotiable.

When it comes to the max compensation, brokers are capped at 2.75%. This is actually really good because most big banks or retail lenders don’t have the same cap. Some big banks go up to 4-5%! This is yet another reason big banks are bad for your wealth. So you may be thinking that going with a bank like Chase or Wells Fargo would be saving you money, but in the end you could be spending more money than if you had a professional mortgage broker on your team.

In the snapshot of the closing cost details, you can see the first section is the Origination Charges. This is where the broker is paid. It is also where you will find any points paid to the lender. I’ll explain points later. Notice in this snapshot, the broker was paid by the lender and not the borrower. In this instance, the broker for me was like the Realtor, free to use to find the best deals!

In Section B, you find the fees that are dictated by the lender. This is an area, along with the points, that the broker can help you find the good deals. When looking at various lenders, you might have one with a lower interest rate, but you have to pay points (a percentage of the loan). Another company may have much higher closing costs, but the same interest rate. It may be beneficial to pay the points because the points amount is lower than the difference in the loan cost. A mortgage broker will walk you though all of that.

Disclaimer

Once again, I am not a financial advisor. These tips are some things I have validated with my own personal experiences. If you feel you need more personal advice, please consult a professional financial advisor. Dont forget to check out the Book List for published authors on this topic!

{kind=link}

{kind=link}

{kind=link}

{kind=link}