So My Company Offers a Retirement Account

Contributing to a retirement account is one of the smartest things you could do. But, when you look at your options, you see a Traditional and a Roth account. What are the differences? What should you choose? Well the first step is to understand the difference between the two accounts. Understanding these will help you with your unique situation. The difference comes down to Pre-Tax and Post-Tax

Traditional Retirement Account

This is the most common understanding retirement account. Your company may offer a 401K with or without matching. Traditionally, you would contribute pre-tax money into this retirement account. If your company was a good one, they would match a certain percent. As I said, this is PRE-TAX. But, what does that mean? It means, before the government taxes your income (social security, medicare, etc.) funds are moved to your retirement account. So, if you made $1000 and you contribute $100 to your traditional retirement account, the government will only tax the $900 of remaining income.

Now, before you think that the money is tax free, I want to explain how the government gets it’s money. The money is taxed when you withdrawal the money. If that $100 grew to $10,000 over time and you went to withdrawal money after you retire, you will be taxed on each withdrawal you take. So, instead of being taxed on that $100, you’ll be taxed on the $10,000 on each distribution.

Roth Retirement Account

This retirement account differs from the traditional by how the taxes are handled. In the $1000 scenario, the government would tax the full $1000. After, $100 would go into your retirement account. The money in the account has already been taxed and is free to grow. This is similar to a regular mutual fund, as it is POST-TAX and grows with your selected investments. However, these funds are not able to be withdrawn until retirement.

Now, the best part, is when the funds are withdrawn, they are tax free. That means if that $100 grows to $10,000, it is distributed tax free. You paid tax on the $100 not the $10,000. If it seems too good to be true, I don’t blame you. One thing is there are contribution limits that prevent people from taking too much advantage of this retirement account type.

Understanding Tax Brackets

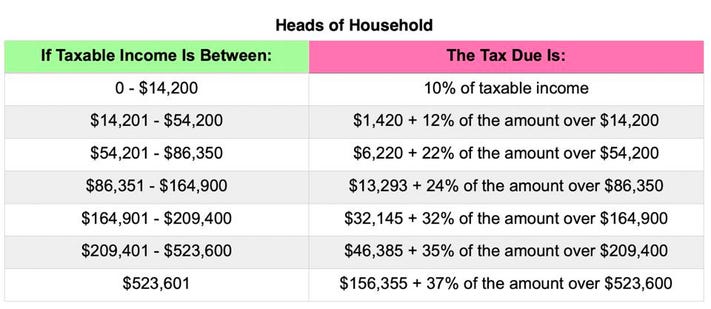

One of the largest consideration you should take when choosing a retirement account is the tax brackets. If you look at the following table, you can see how much your income is taxed. The thing with traditional is you are banking that you’re going to have a lower tax bracket for the funds when you withdrawal them. If you make $210,000 a year, you might consider putting some money in a traditional account to lower your tax bracket. You’re assuming that when you retire, your tax bracket will be way lower, based on your distributions.

When you’re younger, and being taxed in a low tax bracket, it is recommended that you contribute more to a Roth retirement account. It is better to be taxed 12% on $100 vs. 24% on the money that it may turn into.

Which to Choose?

Contributing to a retirement account is one of the best “invest in yourself” methods you can do. The government gives huge benefits to these accounts because these are funds that keep the economy going. Take full advantage of your company’s contribution matching, because that is free money. Some times, your company will match using traditional funds when you contribute to your Roth. You just need to check out your company’s policies.

Disclaimer

Once again, I am not a financial advisor. These tips are some things I have validated with my own personal experiences. If you feel you need more personal advice, please consult a professional financial advisor. Dont forget to check out the Book List for published authors on this topic!

{kind=link}

{kind=link}