Understanding Compounding is Critical to Financial Success

This article dives into what is meant by understanding compounding and compound interest. I will explain how frequency increases the amount of money you can make on your money. I will dive a little bit into the math behind it, but just know that higher interest rates compounding more often mean more money in your pocket.

What is Compounding?

In simple terms, compounding (in this case, compound interest) is the amount of money that is applied to the balance over a set period of time applied at set intervals. Ok, that may not have been so simple, but let me explain. If you have $100 and the interest rate is 1%. This means the interest is $1 (1% of $100). Now, if this interest was compounded annually, that means the 1% would be added to the balance every year. So, at the end of year one, you would have $101. Are you following? Now, compounding is refers to how your next interest payment. As I said, it compounds annually. So, now that you have $101, the interest is $1.01. After the second year, you now have $102.01. This is a 2.01% increase from your initial $100 balance.

Understanding Compounding Frequency

In the example in the previous section, the nominal annual interest rate was 1% and it compounded annually. The interest rate does not have to compound annually, in fact, it could compound quarterly, monthly, or even daily. This works by dividing the APY by the amount of times it compounds within the year. Say in the previous example the interest compounded monthly. The 1% would be divided by the 12 months (0.083% a month). This would result in the first month having an interest payment of $0.083. At the end of the first year, the balance would be $101.01. The actual percentage is 1.005% [commonly referred to as the Annual Percentage Yield (APY)]. As you can see, the more often the balance is compounded, the more yield you’re seeing. This is all because of compounding.

Compounding Math

Ok. This is probably the worst part for most people, the math, but it is necessary to understand compounding. I know for many of us, we just want to know the overall explanation of how it works, no need to get into the needy gritty. Just stick with me in case you need to use this math in programs such as Excel.

APY = (1 + inom/N)N – 1

In this equation, inom is the nominal interest rate, or the rate that was originally listed for an annual interest rate, and N is the number of times the amount is compounded per year. In the example, inom was 1% and N was 12. Using this equation, you can solve that the APY is (1+1%/12)12 – 1 = 1.005%. As you can imaging, on a larger scale, the extra boost to the percentage would have a greater effect on the balance. This also shows why the a higher interest rate could add more to your balance. Think about this when you read why big banks are bad.

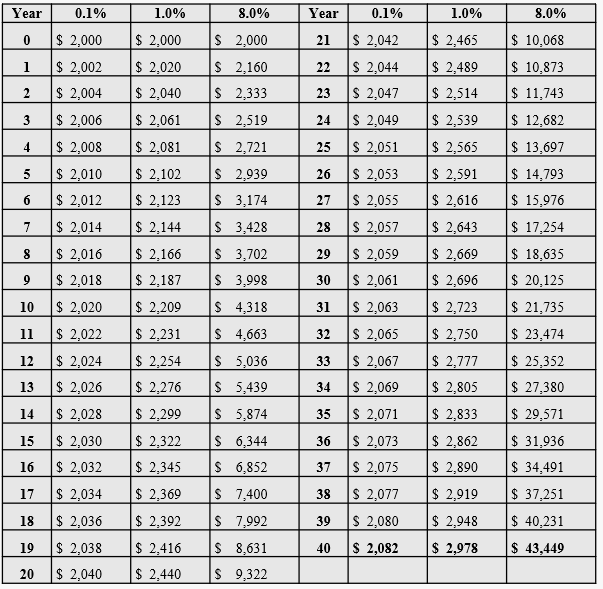

Compounding from $2K to $40K

Without further ado, let me show you how a $2K balance with the interest rate compounded annually brings you to a balance of $2,082 or $43,449 over the course of a 40 year career. Below, the table shows the interest rates of 0.1% (big bank highs), 1% (from the example), or 8% (the average rate of return from the stock market). As you can see, with the 8% annual return on investment (ROI), you can significantly increase your money over the course of your career.

{kind=link}

{kind=link}