WTF is Credit

Understanding credit and how it is used by creditors is incredibly important to building your financial foundation. If you look to buy a car, a house, or take advantage of any type of credit program, you need to build credit. Below I attack some myths to credit and show you how you can build your credit rating. Follow along on YouTube if you hate reading as much as I do (engineer math geek).

Understanding Credit Myths

There are a bunch of myths that I heard regarding credit that could derail you from achieving great credit and also cost you money. Most of these myths I learned from my mother. While she knew the importance of credit in life, she used it very poorly. This may be why I have almost always had a better credit rating than her.

Myth 1: You Should Carry A Balance

I think this myth comes from the point of reliability. One things creditors want to see is that you can pay your bills on-time. This can be your car payment, loan payment, or credit card payment. The myth, however, is that holding a balance, even a small one, on your credit card helps your credit. This is FALSE! The credit card companies do like when you do this, but only because that is how they make money off of card holders. You should never, if you can help it, leave a balance on your credit card because it is giving away your hard earned money.

Myth 2: Close Your Accounts When Not Using Them

This myth comes with the fun image of someone cutting up their credit card with scissors. The myth is once you’re done using a line of credit for good, you should cut the card and close the account so you never use the card again. Sounds good right? Not necessarily. I will explain later why closing the account can hurt you.

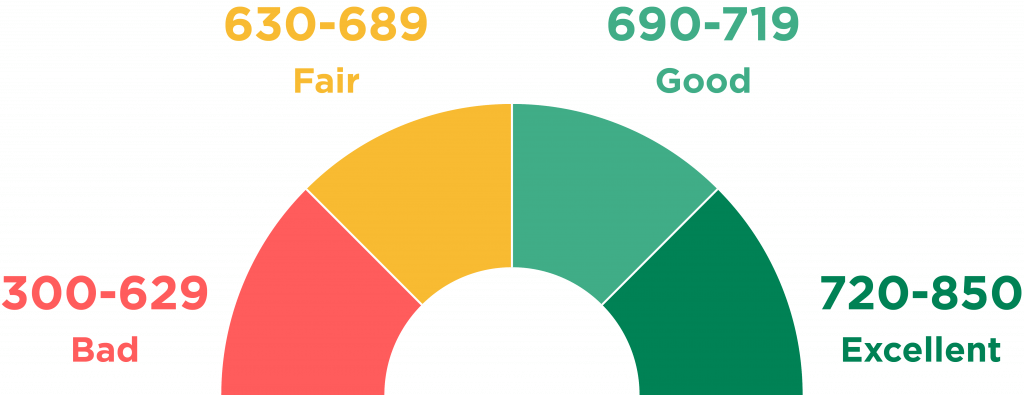

Understanding Credit: Credit Score

I have said this many times, especially when talking about building you financial foundation, that your credit score is like the shell of a car. You may be presented with a brand new sports car, but there is so much more to the car than meets the eye. What type of engine does it have? How is the torque? All of these other factors determine whether its a $20,000 base model or the $100,000 premium model. The credit score is the same. The following factors are the meat and potatoes, the substance that goes into your overall credit rating.

Understanding Credit: Total Credit

First of all, I want to point out that your total credit has absolutely nothing to do with how much money you have in your bank accounts. You can have $100,000 in your bank account, but if you don’t have any credit, you’re not likely to get approved for any financing. Total credit is the sum of all lines of credit you have open. So, to get this number, combine the max credit from each of your credit cards. If you have a credit card with a $1,000 limit and one with a $2,000 limit, you will have a total credit of $3,000. This piece comes into play in two ways. First, the total credit helps when looking to finance big purchases. The second ties into the next piece, available credit.

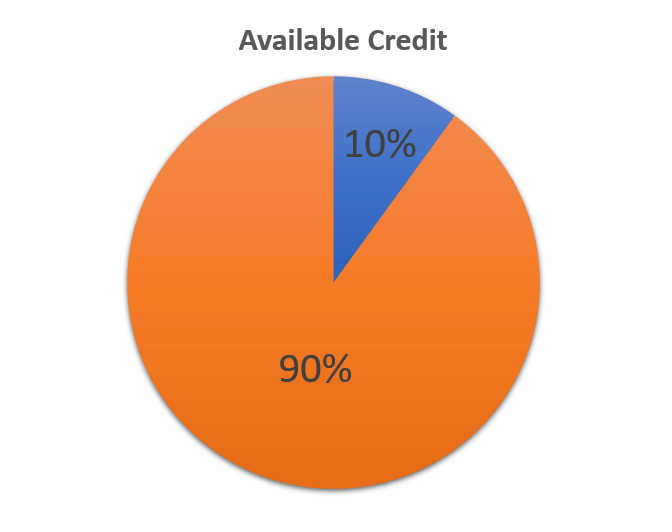

Understanding Credit: Available Credit

Available credit is how much money you have against your accounts divided by the total credit. So, if you purchased a $100 item using your $1,000 limit credit card, you now have 90% available credit (100/1000 = 10%). This is one reason why total credit is so important. This example of 90% is not too bad right, but what if your available credit was 20%? That does not look good. This could be because you bought an $800 computer on your $1,000 credit card. If you had a $10,000 limit instead, you would have used 8% instead of 80%; therefore, you would have 98% available credit. Much better!

Understanding Credit: Credit History

The third major piece to your credit rating is your credit history. As I said in the Financial Foundation post, there are two main ways I considered to build your credit history. A secure credit card and a savings builder loan will get your history off the ground. Consider you credit history like a stopwatch. The second you start a line of credit, the watch starts. It ticks away until you close the account. The longer the time one the watch, the better the history. This is one reason why closing an account is bad. You hit stop on the watch forever. Also, that deducts from your total credit, so two dings. Of course, you dont always want to keep something open that has an annual fee, but that is something to consider. Anyways, you should consider starting your credit history as soon as possible using the two methods I suggested.

Understanding Credit: Other Considerations

There are other pieces that can ding your credit, but not as much as the three I just presented. I get dings on my credit for having balances on too many lines of credit. This will be explained in future blog posts when I discuss using credit cards to make money. I also get dinged from having too many credit inquiries. This ding happens any time a creditor looks at your credit rating. This ding disappears after a few months or so. If you are looking for a home loan, you will get the ding for the first inquiry; however, if you shop to multiple vendors, the dings are consolidated into one, so it wont hurt to shop around.

Tips and Tricks

There are lots of tips and tricks that have helped me get to and stay in the top credit rating.

- Start Early. As I said, the sooner you start, the sooner you build that credit history

- Ask for Increases. Call your credit card companies every 6 months and ask for an audacious increase in your credit. I used to ask for $10,000 max, even though my current limit was under $5,000. They would tell me I was preapproved for something lower. I would take it, then wait another 6 months to try it again. Worked until I hit a ceiling of over $100,000. My income wouldn’t allow for anything higher

- Never Carry a Balance on Your Credit Card. This will keep you available balance in check and also save you money by not paying any interest on your credit cards

Disclaimer

Once again, I am not a financial advisor. These tips are some things I have validated with my own personal experiences. If you feel you need more personal advice, please consult a professional financial advisor.

{kind=link}

{kind=link}